Www What Is Best Interest Rate for Gst to Lock the Money in the Td Bank in Canada

THE CURRENT SITUATION

Very Low Mortgage Rates

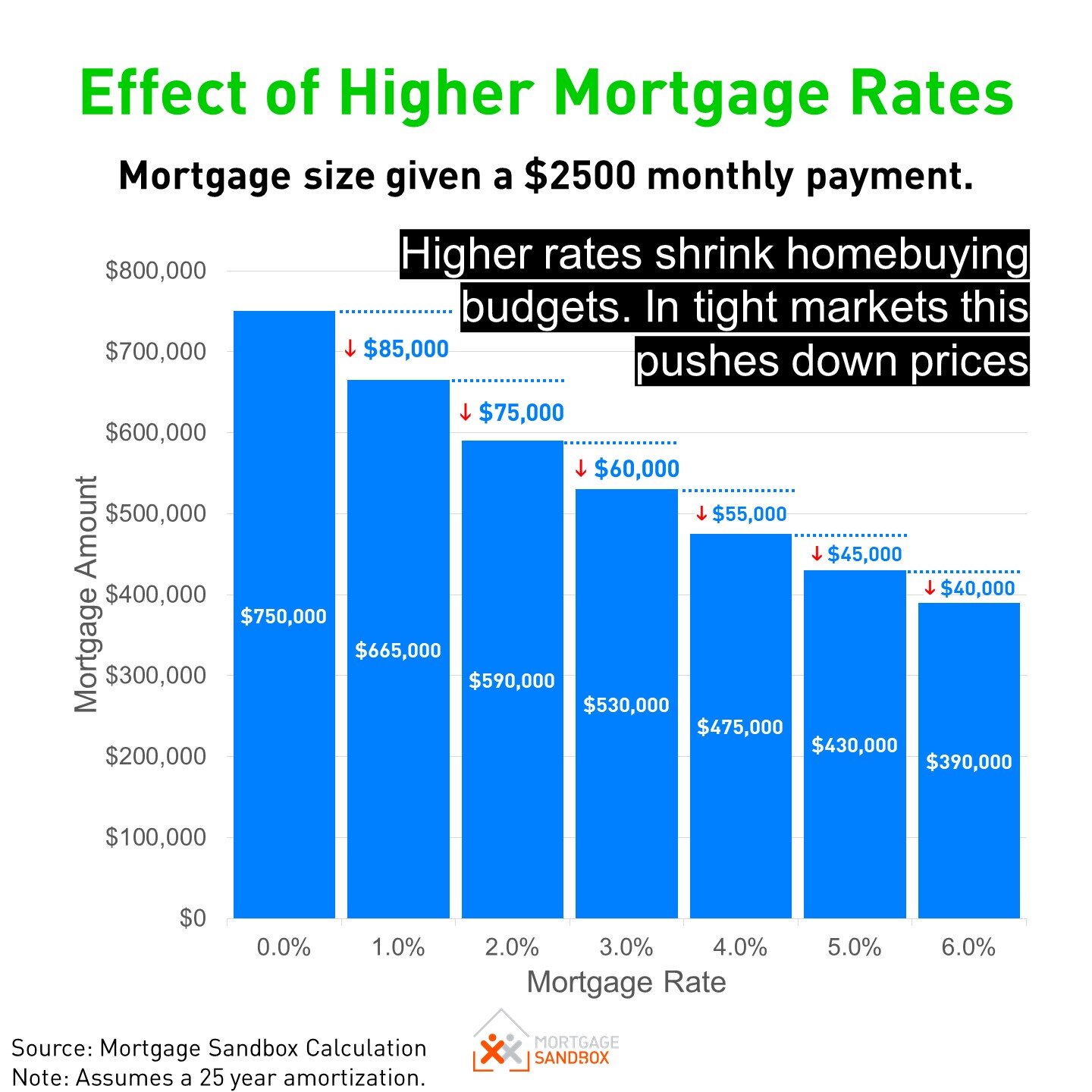

Fixed rates have risen between 1% and 1.v% from the pandemic-induced record lows, and they are expected to go along rising. As mortgage rates rising, they reduce homebuying budgets.

The touch of early rate increases on homebuying budgets will be greater than the subsequent charge per unit increases.

Prospective homebuyers can accept advantage of this effect by getting a pre-approved mortgage 4 months before making a purchase. By the time they notice a place they similar, rates may have risen, and competing bidders who didn't get a pre-canonical committed charge per unit might exist saddled with smaller homebuying budgets.

If your bank doesn't offering a four-calendar month rate guarantee with their pre-blessing, then talk to a mortgage broker.

MORTGAGE RATE FORECASTS

Should I Lock in a 5-Yr Fixed Rate?

Banks accuse extra involvement for the privilege of borrowing at a fixed rate. Usually, they charge more the longer the rate is locked in. Is information technology worth paying extra for their fixed-rate service?

Locking in a iii.30% 5-year fixed mortgage charge per unit will simply start benefiting you lot financially if variable rates continue to climb. Variable rates are expected to ascent roughly 1 per centum over the course of 2022.

I have a variable rate today. Should I lock in now or expect?

Nearly variable-charge per unit mortgages permit y'all to lock in someday. Should you? If you desire the security of a locked-in charge per unit, locking-in now seems prudent. Stock-still rates have been rising and are expected to ascension further.

Fixed-rates Provide Peace of Listen

If the hazard of ascent rates worries you, then you should consider a fixed-rate mortgage rate term. Locking in your rate provides peace of mind, but it does come up with some risks that many people aren't aware of.

Fixed-rates Have College Counterfoil Penalties

Suppose you lot are planning to sell or move in the side by side few years. In that case, cancelling a fixed-charge per unit mortgage before completing the total term can result in a significant penalisation fee.

Shall I Get A Variable Rate Mortgage?

Variable rates are typically a little lower than fixed rates because the borrower takes on the chance of rates changing over time.

Variable rates are expected to remain below 3 percentage well into 2023. That'south pretty low, but it is however possible to lock in a 5-yr guaranteed stock-still rate lower than 3 percentage today.

HOW FORECASTS Work

Forecasts are built on assumptions, and then naturally, unlike assumptions near what will happen atomic number 82 to dissimilar forecast results. That is why Mortgage Sandbox publishes the range of projections and the average of all the forecasted rates.

Apart from the economic assumptions, there is also guidance from the Bank of Canada. The Bank interferes in markets to push rates below the level that the free market would set. Often, Banking company guidance is more important than the economic fundamentals when it comes to rates.

Forecast Assumptions

A Weak and Improving Economy

Canada is now climbing out of a deep recession and nosotros are transitioning to life with COVID. COVID volition e'er be in apportionment, similar the flu, and nosotros volition need to become regular vaccinations to protect us from new variants.

Rising Mortgage Rates

The Bank of Canada projects that inflation will non reach a consistent 2% until one-time in 2023. They believe the electric current run-up in inflation is due to supply-chain constraints and is non a long-term systemic event. Eventually, the Bank of Canada will work toward raising rates to the 'neutral range.'

The Bank Rate is well below what would be considered a neutral range. According to the Bank of Canada, the "Governing Council continues to estimate that the policy interest rate volition demand to rise over time into a neutral range to achieve the aggrandizement target." This policy implies that once Canada emerges from a recession, rates will begin to ascent.

Read: Why is the Bank of Canada increasing your borrowing costs?

Forecast Foundations

Fixed-Rate Mortgage

The foundation for a 5-year stock-still-rate mortgage forecast is the 5-twelvemonth government of Canada bond, and the government is considered a riskless borrower.

Mortgage loans are considered low risk but riskier than loans to the authorities. And so the average Canadian has to pay 1.5 to 2 percent more on a mortgage than the government pays to borrow money. The spread or gap betwixt the authorities borrowing rate and some other loan charge per unit is called a 'run a risk premium.'

Currently, bail rates are rising, then if the risk premium remains unchanged, we should expect that mortgage rates will begin to ascent.

KEY TAKEAWAYS

Our advice is to speak to a Mortgage Broker as early equally possible to lock in a rate. Y'all can lock in your mortgage charge per unit upwards to 120 days before closing on a home buy or the renewal of your mortgage.

Here's our mortgage renewal guide that volition aid y'all navigate the process.

Is information technology a better time to Purchase or Sell a home?

There are more than economic factors on balance, putting downward pressure level on dwelling house prices than upward pressure.

However, that was also the instance during the pandemic when consumer sentiment drove the market place to tape highs in near every Canadian urban center.

-

If you believe that the rise in buying activity is explained by Canadians seeking more living space, and so the terminate of pandemic restrictions coming this summer might trigger an end to this economic existent estate bicycle.

-

If you believe that involvement rates are the chief driver of dwelling house prices, then the forecasted rising in rates would indicate prices will moderate in the 2d one-half of 2022.

-

If people can piece of work from home then the urban housing supply constraints are lessened - so the structural supply shortage is less of a factor today than before the pandemic.

Homebuyer Advice

If you program to buy in the next three years, be mindful that in that location is a risk that prices volition fall in the short run, and then fix yourself for that possibility. It is also possible prices could continue to rise by +ten% annually but that seems less likely.

The ascension mortgage rates provide less purchasing power for buyers than 6 months agone.

Abode Seller Communication

If you were planning to sell, then it may exist worthwhile selling sooner than later. Although the pandemic has caused tape-breaking market conditions, at that place is a lot of dubiousness surrounding how conditions will change once the pandemic is over.

Like this study? Like us on Facebook .

Canadian Existent Estate Forecasts

Toronto

Real Manor Trends and Forecast

Montreal

Real Estate Trends and Forecast

Hamilton-Burlington

Real Estate Trends and forecast

Victoria

Existent Estate Trends and Forecast

Vancouver

Real Estate Trends and Forecast

Ottawa

Real Estate Trends and forecast

Calgary

Real Estate Trends and Forecast

Edmonton

Existent Estate Trends and Forecast

London, ON

Real Estate Trends and Forecast

Source: https://www.mortgagesandbox.com/mortgage-interest-rate-forecast/

0 Response to "Www What Is Best Interest Rate for Gst to Lock the Money in the Td Bank in Canada"

Post a Comment